Avoid Leaving Value on the Table: Choice of Entity Post-Tax Reform

“The Tax Cuts and Jobs Act, the most sweeping federal tax law change in 30 years”

The Tax Cuts and Jobs Act, the most sweeping federal tax law change in 30 years, has brought with it a myriad of provisions significantly impacting the business community. Many of these provisions, which have an effective date of January 1, 2018, can impact a firm’s economic situation but perhaps none more materially than the new 21% permanent flat tax rate for C corporations and the 20% deduction for qualified business income (QBI).

Effective January 1, 2018, the corporate income tax rate has dropped 14% (from 35% to 21%) compared to 2017, while the top individual rate effective for pass-through entities (LLCs, Partnerships and S Corps) has only dropped 2.6% (from 39.6% to 37%), or 10% with the incorporation of the 20% Section 199A QBI deduction (39.6% versus 29.6%). For good reason, these changes have prompted tax professionals, investors and business owners to reassess their business entity structure. Simply put, the math has changed.

The question we have received frequently from our clients is “should I switch my pass-through entity to a C corporation” or “is a C corporation still the most optimal entity choice”? Fortunately, this is the right question to be asking but one that requires careful consideration.

Let’s look at the math…

The Math – Cash, Cash, Cash

In order to understand the relationship between a pass-through entity and a C corporation, we have modeled two simplified scenarios comparing the overall tax obligation for these two entity choices at varying levels of income. As the math depicts, the optimal entity is in many ways driven by the cash needs of the entity and/or shareholder.

(In these examples, we assume the pass-through entity has elected to be treated as an S corporation and that both the pass-through entity and C corporation are owned by a single owner taking a $50,000 salary who is actively involved. The output shown below includes the impact of federal payroll, self-employment and income taxes.)

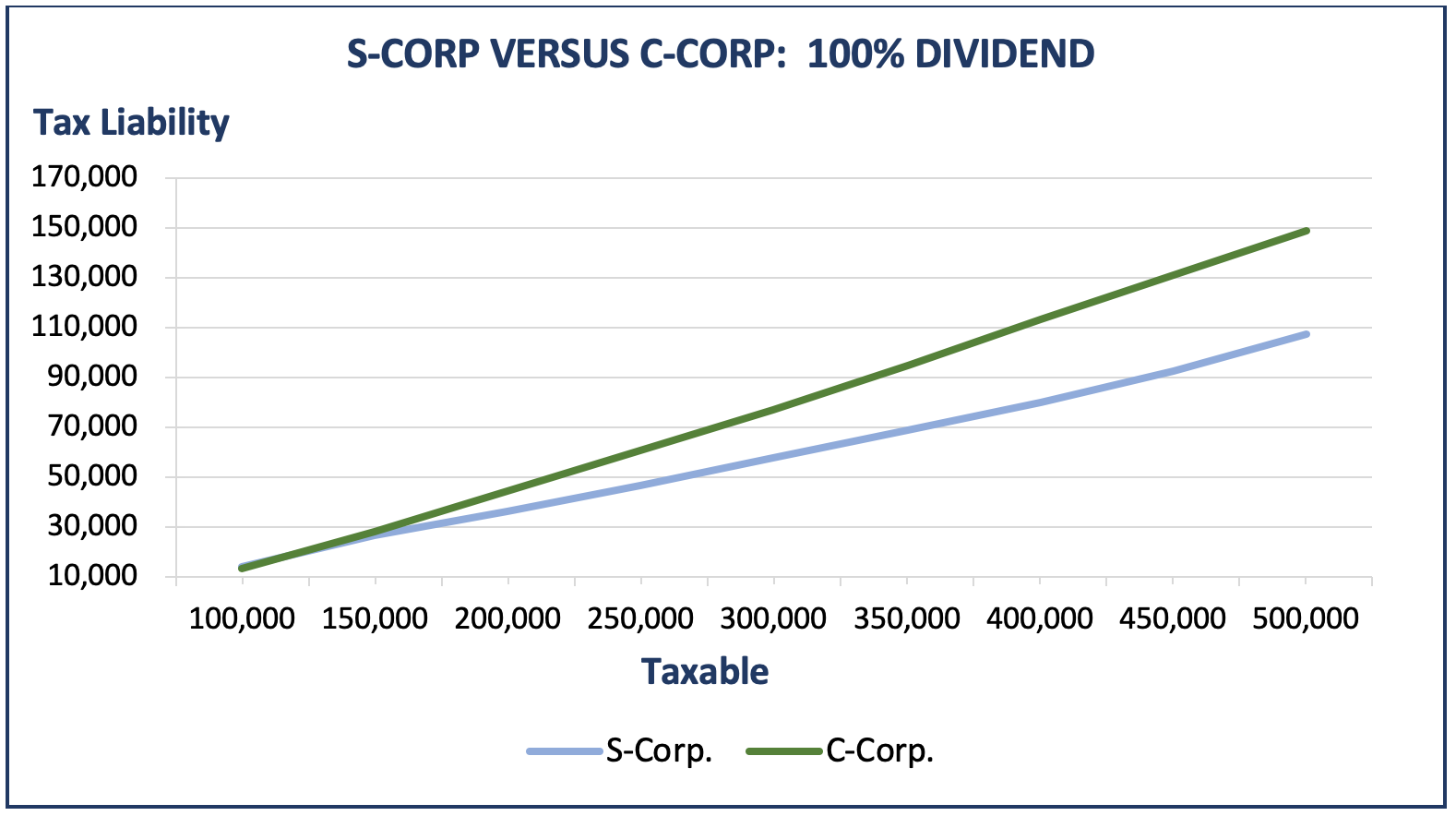

Scenario 1: All Corporate Earnings Distributed through Dividend

This scenario represents a situation where the corporation distributes 100% of its earnings to the shareholder(s) in the form of a dividend. This distribution triggers a “double-taxation” both at the corporate level and individual level. As seen below, for example, at $300,000 of income, the S corporation generates $20,000 of annual tax savings compared to the C corporation. This equates to approximately 7% of additional pass-through income for the S corporation.

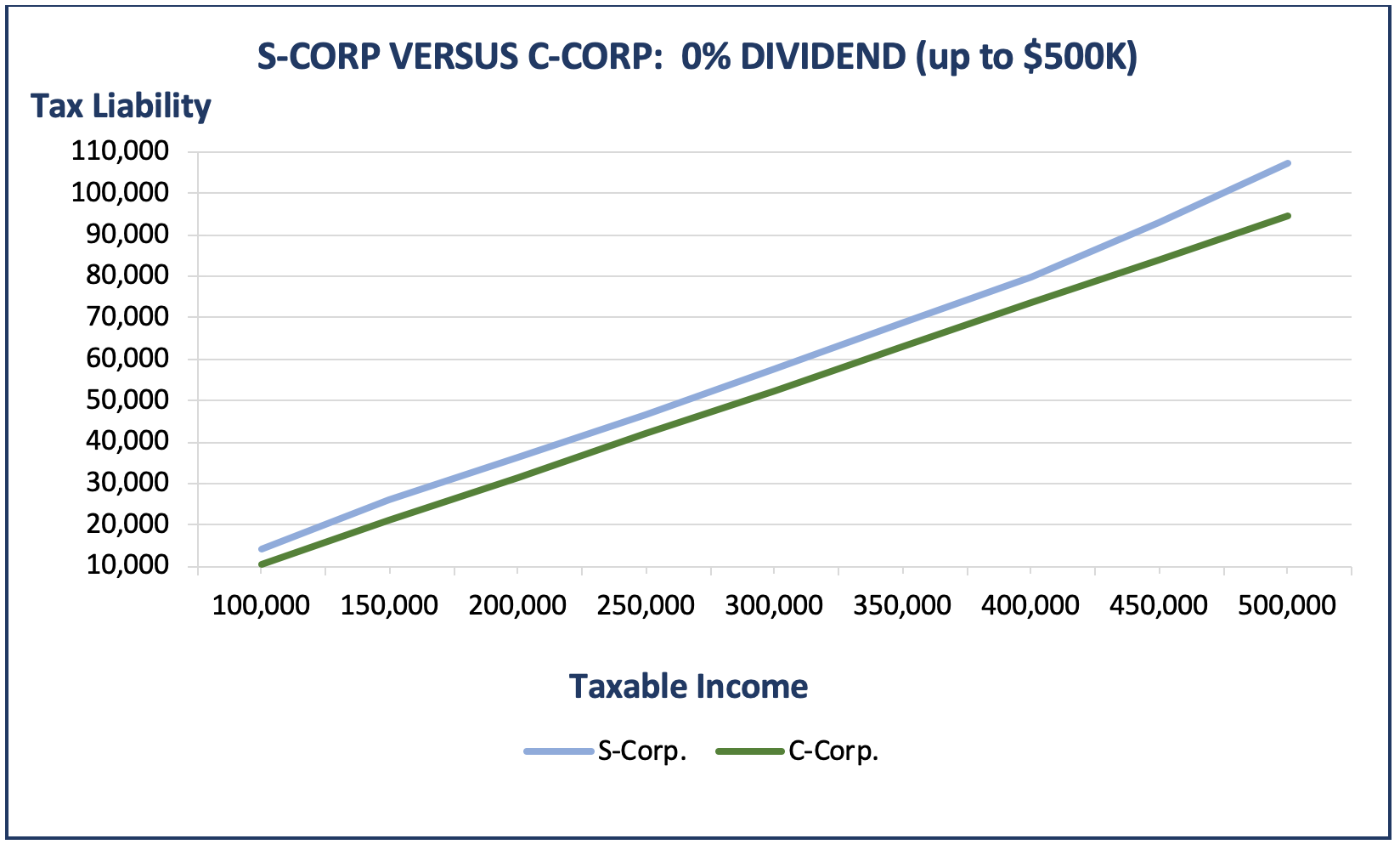

Scenario 2: All Corporate Earnings Retained within the Corporation

Alternatively, this scenario represents a situation where the corporation is in a growth phase or at some part in its business cycle where shareholder distributions are not a priority. In this scenario, 100% of the earnings are retained within the entity. This results in an effective tax rate of 21% for the corporation versus a top individual tax rate for the pass-through income of 29.6% (top 37% tax rate less 20% QBI deduction). As you can see below, for example, at $300,000 of income, the C corporation generates $5,000 of annual tax savings compared to the C corporation. This equates to approximately 2% of after-tax income for the C corporation.

More than Cash

In addition to understanding a firm’s liquidity requirements, each entity should also have a firm grasp on their long-term tax strategy in the context of their unique facts and circumstances. Any change is entity brings with it long-term implications. Additional items that should be considered when contemplating a change include:

State and Local Taxes– The $10,000 cap on state income taxes at the individual level can limit tax efficiency compared to a C corporation which does not have limits on deductibility.

20% QBI Deduction– Understanding the applicability and the extent to which a firm can take advantage of this deduction will have a significant impact the comparison of the differing types of entity choices (see separate article on the 199A Deduction here).

Use of Firm Earnings– Optimizing the use of the firm’s earnings can impact the choice of business entity. Firms that are evaluation investment opportunities should consider investments within the firm (including personal holdings) and those outside the firm and then determine if greater value can be manufactured through appropriate entity selection. Be sure to consider PHC tax Under Section 541.

Built-In Gains Tax (“BIG” tax)- Although an S corporation is normally not subject to tax, when a C corporation converts to S corporation status, the tax law imposes a 21% tax on the net, recognized built-in gains of the corporation. The idea is to prevent the use of an S election to escape tax at the corporate level on the appreciation that occurred while the corporation was a C corporation. This tax is imposed when the built-in gains are recognized (i.e., the appreciated assets are sold or otherwise disposed of) during the five-year period after the S election takes effect.

Accounting Methods– When a pass-through entity elects to be treated as a C-Corporation, the entity may be required to use the accrual method of accounting. Beginning in 2018, C corporations and partnerships with C corporation partners may use the cash method of accounting if their annual average gross receipts that do not exceed $25 million for the prior three years, regardless of whether the purchase, production, or sale of merchandise is an income-producing factor. However, S corporations and partnerships are allowed to use the cash method without regard to whether they meet the $25 million gross receipts test, so long as the cash method clearly reflects income. In most cases, the change from cash to accrual is a costly tax change. Because of this, under Sec. 481(d)(1), the IRS allows change to be spread out over a 6-year period.

A Firm’s Exit Strategy– the double taxation associated with the sale of assets within a C corporation can significantly reduce the value of the transaction. Firms should understand the impact of entity choice on potential future asset and stocks sales and liquidations.

Passive Investment Income Tax– Firm’s should be aware that if a corporation has any “earnings and profits” and subsequently elects S corporation status, it may be subject to a corporate-level tax on its passive investment income. This tax would apply in any year the S corporation’s passive investment income exceeds 25% of its gross receipts. If that happens, the net passive income (after applicable deductions) that exceeds 25% of gross receipts is taxed at the highest corporate tax rate (21%).

How Can We Help

So where should you begin? With a well thought out game plan and with the appropriate team members in place, the determination of the appropriate choice of entity can be a rewarding process. Tax reform has provided entities with a unique, once-in-a-lifetime opportunity to take advantage of favorable tax rates and incentives intended to stimulate long-term enterprise growth. At Midcoast, our team of expert advisors can assist you with the development and implementation of a game plan to achieve these results so that you can move forward with a high degree of confidence that you are not leaving value on the table.