House Passes "Cares Act": What the Small Business Owner Must Know

The Coronavirus Aid, Relief, and Economic Security (“CARES Act”), a $2 trillion emergency bill that Congress has prepared in response to the Coronavirus (COVID-19) pandemic, was passed by the Senate on March 25, 2020, was passed by the House today, March 27, 2020 and President Trump is expected to sign with little delay. Many of the provisions of this bill provide financial relief to both individuals and small business. A summary of these provisions is being provided below in order to ensure you are informed on the progress of this bill of how these provisions may impact you as an individual and a small business owner. We have organized this article into four main components:

1.) The Paycheck Protection Loan Program,

2.) SBA Loan Relief,

3.) Tax Incentives, and

4.) Unemployment Insurance

Paycheck Protection Loan Program

The CARES Act creates a “Paycheck Protection Program” for, among others, small employers with 500 employees or fewer, those that meet the current Small Business Administration (“SBA”) size standards, self-employed individuals, “gig economy” individuals and certain nonprofits. The program is intended to prevent economic hardship due to economic losses caused by the COVID-19 pandemic. The program would provide 8 weeks of cash-flow assistance through 100 percent federally guaranteed loans to small employers who maintain their payroll during this emergency. If the employer maintains payroll, the portion of the loans used for covered payroll costs, interest on mortgage obligations, rent, and utilities would be forgiven, which would help workers to remain employed and affected small businesses and our economy to recover quickly from this crisis. This proposal would be retroactive to February 15, 2020, to help bring workers who may have already been laid off back onto payrolls.

Special Loan Terms

The Paycheck Protection Program which, expands the SBA’s loan program by expanding the capability to borrow funds for eligible expenses include payroll support, such as employee salaries, paid sick or medical leave, insurance premiums, and mortgage, rent, and utility payments. In addition, key provisions of the program are detailed below:

- The size of the loans would equal 250 percent of an employer’s average monthly payroll

- Covered payroll costs include salary, wages, and payment of cash tips (up to an annual rate of pay of $100,000); employee group health care benefits, including insurance premiums; retirement contributions; and covered leave

- The maximum loan amount would be $10 million

- The cost of participation in the program would be reduced for both borrowers and lenders by providing fee waivers, an automatic deferment of payments for one year, and no prepayment penalties

- Complete deferment of loan payments for at least six months and not more than a year

- Loans would be available immediately through more than 800 existing SBA-certified lenders, including banks, credit unions, and other financial institutions

- Ensures borrowers are not charged any prepayment fees.

- SBA would be required to streamline the process to bring additional lenders into the program. The Treasury Secretary would be authorized to expedite the addition of new lenders and make further enhancements to quickly expedite delivery of capital to small employers

Loan Forgiveness

The program establishes that the borrower shall be eligible for loan forgiveness equal to the amount spent by the borrower during an 8-week period after the origination date of the loan on payroll costs, interest payment on any mortgage incurred prior to February 15, 2020, rent on any lease in force prior to February 15, 2020, and utilities for which service began before February 15, 2020. The remaining loan balance will have a maturity of not more than 10 years, and the guarantee for that portion of the loan will remain intact.

Amounts forgiven may not exceed the principal amount of the loan, additionally, eligible payroll costs do not include compensation above $100,000 in wages. The amount forgiven will also be reduced proportionally by any reduction in employees retained compared to the prior year and reduced by the reduction in pay of any employee beyond 25 percent of their prior year compensation. To encourage employers to rehire any employees who have already been laid off due to the COVID-19 crisis, borrowers that re-hire workers previously laid off will not be penalized for having a reduced payroll at the beginning of the period.

Canceled indebtedness resulting from this section will not be included in the borrower’s taxable income.

SBA Loan Relief

As part of the CARES Act, $17 billion was provided to implement and loan debt relief program. For six months, SBA is required to pay all principal, interest and fees on all existing SBA “covered loans” starting on the next due date. The CARES Act defines a covered loan as an existing 7(a) (including Community Advantage), 504, or microloan product. Loans that are already on deferment will receive six months of payment by the SBA beginning with the first payment after the deferral period. Loans made up until six months after enactment will also receive a full 6 months of loan payments by the SBA. Additionally, the bill requires that SBA enact these programs with regulations no later than 15 days after the Act is signed into law.

Tax Incentives

One-Time Financial Assistance

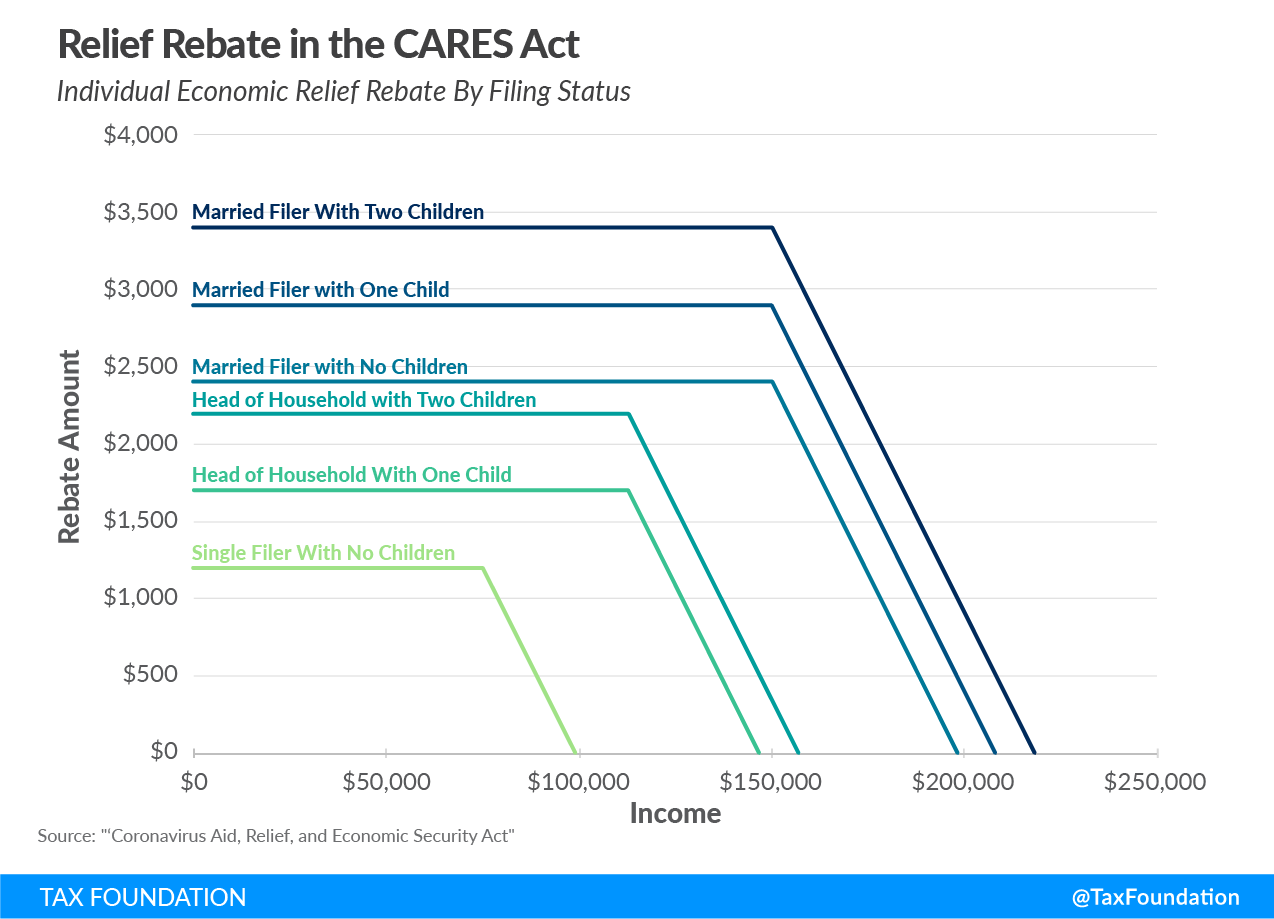

This assistance comes in the form of a one-time tax rebate check of $1,200 per individual and $500 per child for those with a valid SSN. There are no earned income or tax liability requirements to receive these rebate checks. The full credit amount is available for individuals with income at or below $75,000 ($112,500 for heads of household), and couples with income at or below $150,000.

The rebate phases out at $75,000 for singles, $112,500 for heads of household, and $150,000 for joint taxpayers at 5 percent per dollar of qualified income, or $50 per $1,000 earned. It phases out entirely at $99,000 for single taxpayers with no children and $198,000 for joint taxpayers with no children.

The recovery rebates will use 2019 tax returns (2018 if the taxpayer has not filed in 2019) to determine the advanced rebate amount and reconcile the rebate based on 2020 income. This means that taxpayers who receive a smaller rebate than they are eligible for based on 2020 income will receive the difference after filing a 2020 tax return, but overpayments of rebates due to a higher income in 2020 will not be clawed back.

The Table below from the Tax Foundation at taxfoundation.org provides an estimate of the refund based on filing status and estimated income.

Less Stringent Rules on Retirement account Required Minimum Distributions (“RMD”) and Distributions

Certain individuals that are subject to mandatory minimum distributions from their retirement accounts would be able to keep their capital invested instead of being forced to cash out to draw on that capital without penalty, which would be suspended for 2020.

Similarly, the bill also waives the 10% penalty on coronavirus-related early distributions from 401(k)s and IRAs, which applies to distributions made at any time during 2020. Withdrawn amounts are taxable over three years, but taxpayers can recontribute the withdrawn funds into their retirement accounts for three years without affecting retirement account caps. Eligible retirement accounts include individual retirement accounts (IRAs), 401Ks and other qualified trusts, certain deferred compensation plans, and qualified annuities.

Payroll Credit for Furloughed Workers

Employers are eligible for a 50 percent refundable payroll tax credit on wages paid up to $10,000 during the crisis. The credit would be available to employers whose businesses were disrupted due to virus shutdowns and those that had a decrease in gross receipts of 50 percent or more when compared to the same quarter last year. The credit can be claimed for employees who are retained but not currently working due to the crisis for firms with more than 100 employees, and for all employee wages for firms with 100 or fewer employees.

Delays Payroll Tax Payments for Employers

Employers can delay the payment of their 2020 payroll taxes until 2021 and 2022, leading to approximately $300 billion of extra cash flow for businesses. Employers would be allowed to delay until January 1, 2021, with 50 percent owed on December 31, 2021 and the other half owed on December 31, 2022.

Student Loans

Certain employer payments of student loans on behalf of employees are excluded from taxable income. Employers may contribute up to $5,250 annually toward student loans, and the payments would be excluded from an employee’s income.

Restores Supports for Businesses Suffering Losses

The bill also allows businesses to carry back losses from 2018, 2019, and 2020 to the previous 5 years, which will allow businesses access to immediate tax refunds. The NOL limit of 80 percent of taxable income is also suspended, so firms may use NOLs they have to fully offset their taxable income.

Encourages Businesses to Invest in Improvements

The bill would fix cost recovery for investments in Qualified Improvement Properties, which will allow businesses that made these investments in 2018 and 2019 and receive tax refunds now.

Net Interest Deduction Limitation

The net interest deduction limitation, which currently limits businesses’ ability to deduct interest paid on their tax returns to 30 percent of earnings before interest, tax, depreciation, and amortization (EBITDA), has been expanded to 50 percent of EBITDA for 2019 and 2020. This will help businesses increase liquidity if they have debt or must take on more debt during the crisis.

Unemployment Insurance

The unemployment insurance (“UI”) provisions of the CARES Act provide $250 billion for expanded unemployment benefits. These benefits include an additional $600 per week payment to each recipient for up to four months, and extend UI benefits to self-employed workers, independent contractors, and those with limited work history. The federal government will provide temporary full funding of the first week of regular unemployment for states with no waiting period and extend UI benefits for an additional 13 weeks through December 31, 2020 after state UI benefits end. The Act also expands the scope of recipients including those who are self-employed as well as independent contractors. In addition, state and local governments as well as nonprofits can pay unemployment to their employees.

How Can We Help

In the weeks to come, as these changes are put in place, our team will be on standby to support you in implementing these provisions as we navigate this time of uncertainly and financial difficulty. Reach out to one of our advisors today to discuss how these changes may impact your unique situation.

Sources:

Garret, W., LaJoie, T., Li, H., Bunn, B.,Tax Foundation 2020, accessed March 27, 2020.

<https://taxfoundation.org/cares-act-senate-coronavirus-bill-economic-relief-plan/>

U.S. House of Representatives: Ways and Means, 2020, accessed March 27, 2020

<https://gop-waysandmeans.house.gov/the-senate-cares-bill-helping-small-business/>

National Small Business Association, accessed March 27, 2020

<https://nsba.biz/final-language-on-small-business-stimulus>

Midcoast Tax Advisors, LLC,

Copyright © 2020. All rights reserved.